Are cost and price analyses just more bureaucratic red tape, or are they persuasive negotiation tools?

BY CHRISTINA GRAVES

The U.S. federal government is the largest purchaser of goods and services in the world—and adding this customer to your client list can be a game changer.

However, selling to the government requires more than producing a needed product or service. Notably, it requires knowledge of the rigorous and intricate requirements of the Federal Acquisition Regulation (FAR).

Most high-dollar proposals must be accompanied with well-written and adequately supported cost and price analyses. And when used effectively, cost and price analyses are more than mere checkoff items; they are tools for successfully negotiating favorable contract terms and prices. Analysts who successfully harness this skill set and couple well-written price justifications and source selections with FAR-compliant proposals position themselves to have a competitive advantage in one of the most lucrative markets—government contracting.

Cost and price analyses not only demonstrate that an organization did its due diligence to obtain reasonable pricing from its subcontractors and suppliers, it shows that the organization’s submission is practical and represents a fair and reasonable price.

Cost and Price Analyses—Defined and Differentiated

Cost Analysis

Cost analyses evaluate the proposed price by evaluating each individual cost element, such as direct costs[1]—including:

- Direct labor—Costs related to the personnel carrying out the proposed statement of work (SOW). These costs include the hourly wages of employees actually producing the procured products and providing the proposed services and considers the number of hours required to complete the anticipated contractual obligations.

- Direct material—Costs relating to the quantities and types of raw materials, purchased parts, or subassemblies needed to manufacture a product. These expenses include subcontract and vendor costs.

- Other direct costs (ODCs)—Miscellaneous costs that can be charged directly to a final cost object (such as a contract) other than labor and materials. ODCs have a direct, mappable relationship with the expenses incurred and the final cost object generating the expenses. Freight, sales commissions, and travel are examples of ODCs.

- Indirect costs—Costs that cannot be directly associated with a final cost object and are not directly related to production.[2] The two primary categories of indirect costs are:

- Overhead—e.g., rent and utilities costs; and

- General and administrative (G&A) expenses—e.g., accounting and advertising, which benefit the overall business.

Indirect expenses do not have a direct relationship with the expenses incurred and the final cost objectives. Instead, an allocation of the incurred costs is assigned to cost objectives (intermediate and final) on a causal-beneficial basis.

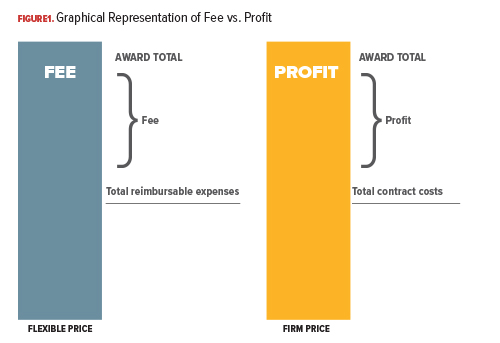

- Fees and profits—

- Fees—The portion of a flexibly priced award that does not pertain to cost reimbursement. Fees represent the arithmetic difference between the total contract price and the total allowable costs.

- Profit—The financial benefit from generating revenues in excess of expenditures. This term pertains to firm-price awards and refers to the portion of the award where the agreed upon price is in excess of contract costs.

Although the terms are slightly different, fees and profit are virtually the same, as shown in FIGURE 1.

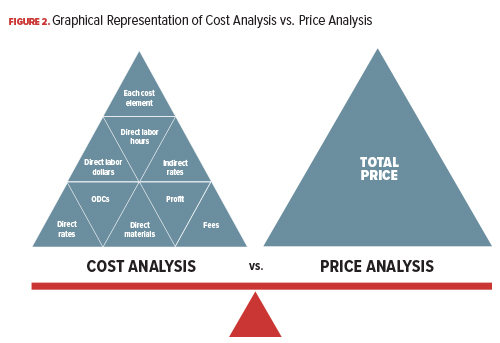

Price Analysis

Price analyses evaluate the reasonableness of the overall award price without evaluating the separate cost elements or profits and fees.[3] The process of price analysis involves a holistic review of the proposed price and aids negotiators in determining if the total contract value is fair and reasonable, regardless of the makeup or distribution of the sum of its costs.

FIGURE 2 highlights the difference between the two analyses.

Regulatory Requirements

As part of the process, and depending on the nature of the procurement, potential government contractors may be required to submit Certified Cost or Pricing Data (COPD).[4] COPD consists of the following:

- Properly completed proposals in accordance with FAR 15.408, Table 15-2, “Instructions for Submitting Cost/Price Proposals When Certified Cost or Pricing Data Is Required”; and

- Cost analyses.

Price analyses are required for all proposals above the FAR’s $10,000 micro-purchase threshold (MPT). They are utilized when cost analyses are not required. Cost analyses are required for all proposals above the $2 million COPD acquisition threshold that do not meet the following FAR 15.403-1(b) exemptions:

- Proposals awarded on the basis of adequate competition,

- Proposals for products and services where the prices are set by law or regulation,

- Proposals for the procurement of commercial items, or

- Proposals that are exempted or waived from this requirement by the head of contracting activity.

It is important to note that COPD must be updated to ensure all negotiating parties have the most current information that a prudent person would deem necessary to make an informed decision. This standard states that, to the best of a person’s knowledge and belief, the COPD provided is accurate, complete, and current as of the date of price negotiations. When events occur that result in a significant change in pricing, contractors have a duty to report this information to the government. For instance, reduced labor costs due to renegotiated union agreements that resulted in lower wages or decreased material costs due to advanced technologies or lower tariffs on imported goods are examples of mandated disclosures. Creating a good initial analysis is a preliminary step. However, refinements and updates are necessary until a final agreed upon price is negotiated.

Potential Penalties

Completing cost and price analyses are a necessary “cost” of doing business with the federal government. Companies must divert resources from their primary focus of providing and selling products and services to researching and implementing government policies. This can be challenging for some organizations due to such things as stretched internal resources, shifting roles of cost analysts and technical professionals, and heightened expectations from oversight organizations such as the Defense Contract Audit Agency (DCAA) and Defense Contract Management Agency (DCMA).

Ensuring compliance with the FAR requires attentiveness, commitment, and diligence. Nevertheless, not adhering to the FAR will result in organizations being bogged down with greater bureaucratic red tape. Failing to provide adequate analyses can result in the following adverse actions:

- Additional audit scrutiny from the government,

- Increased bid and proposal expenses,

- Adverse estimating and purchasing systems audit opinions,

- Mandated percentage of payment withholds,

- Disallowed or decremented proposal costs, and/or

- Delayed or denial of contract and subcontract awards.

Persuasive Negotiation Support

There are positive negotiating externalities to performing adequate cost and price analyses. Consider the following scenario: A potential contractor enters a room and takes a seat, ready to support a position that will cost $3 million to manufacture a part for the Department of Defense (DOD). On the opposite side of the table is a DCAA auditor, eager to show that the DOD should only pay $2 million for the proposed part. And sitting between the two is a DCMA contracting officer ready to enter into a contract on behalf of the government for the amount that is the most adequately supported. (Furthermore, prior purchase history is commonly used to price follow-on contracts. If the potential contractor is unsuccessful and experiences a million-dollar downward adjustment, the price could be locked in for future contracts.)

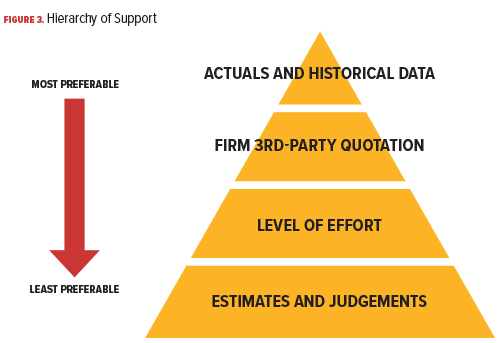

How does the potential contractor defend the $3 million price? This position can be successfully defended with well-written and adequately supported cost and price analyses. Having an itemized listing of the proposed costs substantiated with appropriate documentation is strong evidentiary support that the contractor’s pricing is fair and reasonable. It is difficult to dispute verifiable and factual cost estimating methodologies. Furthermore, the higher up the hierarchy of support, the harder to dispute or question the proposed costs. (Refer to FIGURE 3.)

Continuing with the same scenario, imagine the reason for the million-dollar variance is due to questioned direct material costs. The DCAA auditor asserts the proposed amount is overestimated. However, if the potential contractor is equipped with well-written cost and price analyses that clearly show the proposed direct materials costs are reasonable—and backed up with a comprehensive consolidated bill of materials, which totals the proposed amount; recent purchase orders, which reconcile to proposed material prices; economic indices from reputable organizations, such as the U.S. Bureau of Labor Statistics (BLS); and technical evaluations from experienced engineers and functional specialists, all clearly illustrating that the proposed quantity of parts and types of material are reasonable. Armed with these items, the potential contractor can more clearly present the case for, and increase its chances of entering into a contract with the government for, the targeted amount.

Cost and price analyses can be powerful negotiation tools. It’s essentially “writing across the curriculum” to take analyses and reports originally created to meet regulatory requirements and duel purposing them to also negotiate proposed costs. In the previous hypothetical scenario, the potential contractor, if awarded the contract, would obtain a 33% higher contract value[5] with the assistance of the cost and price analyses than without.

In the same manner that cost and price analyses are effective tools for prime contractors negotiating with the government, they are also effective tools for subcontractors and suppliers negotiating with prime contractors. Using the subcontractors’ and suppliers’ data allows for the determination of a definable fair price. To reiterate, contractors are able to support pricing their goods and services for higher prices and reducing their contract costs as warranted by the data.

Key Considerations: Adaptability and Scalability

Adaptability

As the saying goes, no two people are alike, and this logic applies here as well—no two cost or price analyses are alike. Each analysis should be tailored. The procedures performed for each analysis should depend on the individual supplier’s proposal and estimating practices and industry best practices.

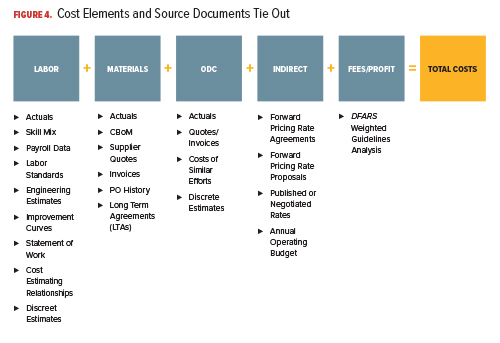

In addition, always keep in mind that these reports also serve the dual purpose of being sound negotiation tools. As such, the components of proposed costs should ideally be broken down with detailed narratives that define the basis of estimates using layman terms. Report narratives should consistently describe the source documents utilized, judgmental factors applied, and assumptions made. Moreover, the narratives should be accompanied by detailed computations—with each variable in the computation of proposed costs having an audit trail mapping it to the estimating source documents (as displayed in FIGURE 4 on page XX).

Scalability

The ability to timely respond to requests for proposals (RFPs) and the capability to successfully navigate surges are key to maintaining market share and remaining competitive. According to the Oak Ridge Institute for Science and Technology, proposals should generally be submitted within four to six weeks after the RFP release.[6] Four to six weeks is a quick turnaround for the magnitude of effort often required to produce FAR-compliant cost and price analyses. The outlay of time and capital often obstructs small contractors’ ability to compete for business. To support this point, consider the following scenario which requires a commitment ranging from 280 hours and $9,333 to 560 hours and $18,667.

Each business day, DOD lists contract awards of $7 million or more.[7] According to this data, on September 24, 2020, the U.S. Air Force awarded 11 contracts ranging from $7.2 billion to $2.2 billion with a median award value of $13.3 million. Assuming the median contract does not meet any of the FAR 15.403-1(b) exemptions, a bidding contractor may be required to complete approximately seven analyses[8] within four to six weeks. Depending on the complexity and size of the award, analyses can take 40 to 80 hours to complete. Assuming a 40-hour standard work week and minimally complex supplier proposal, the ability to meet this demand in four weeks requires two full-time equivalent (FTE) employees. However, a fairly complex supplier proposal requires four FTE employees, as illustrated in FIGURE 5.

Unfortunately, many contractors, especially small businesses, cannot afford to hire a staff of FTE cost analysts and estimators and often forgo these types of opportunities. According to the BLS, the median pay of a cost analyst or estimator is $64,000 annually.[9] Using the U.S. Air Force example, it would cost from $9,333 to $18,667 to produce seven cost and price analyses[10] in order to compete for a $13.3 million sole-source Air Force award. (Further, it should be noted that if these are salaried employees, then the contractor must pay annual salaries from $128,000 ($64,000 * 2 employees) to $256,000.[11] Nevertheless, winning the contract award would result in a significant return on investment.

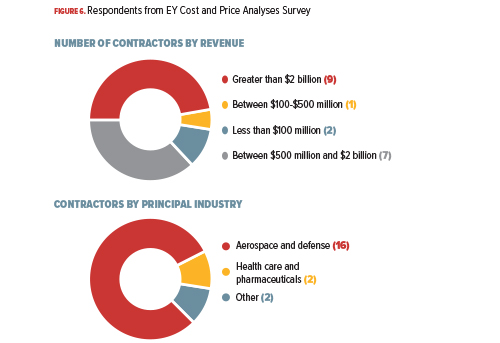

To put this into perspective, Ernst & Young (EY) recently conducted a survey on cost and price analyses compiling the responses of 20 globally recognized organizations. (Refer to FIGURE 6.) Prominent survey results are as follows:

- Respondents completed the following number of cost analyses: 1–5 analyses for 24%, 26–75 analyses for 24%, 76–125 analyses for 18%, and 125+ analyses for 35%;

- Respondents completed the following number of price analyses: 1–50 analyses for 18%, 51–100 analyses for 24%, 101–150 analyses for 6%, and 150+ analyses for 53%;

- Respondents’ average turnaround time for cost analyses is 1–15 days for 21%, 16–30 days for 29%, 31–60 days for 29%, and 60+ days for 21%;

- Respondents’ average turnaround time for price analyses is 1–15 days for 50%, 16–30 days for 14%, and 31–60 days for 36%;

- The number of individuals performing cost analyses is 1–30 individuals for 82%, 31–50 individuals for 6%, and 50+ individuals for 12%; and

- The number of individuals performing price analyses is 1–30 individuals for 59%, 31–50 individuals for 24%, and 50+ individuals for 18%.

Conclusion

The law requires that contractors comply with the FAR, and FAR 15.403-1(b) mandates that defense costs greater than $2 million are supported by accurate, complete, and current COPD. Cost/price analyses have a direct impact on the potential outcome of U.S. government audits, including pre-award and post-award audits. President Donald Trump signed the National Defense Authorization Act Fiscal Year 2019,[12] which increased DOD spending by approximately $160 billion.[13] While government spending is increasing, the citizenry are increasingly calling for greater accountability and oversight on the spending of public funds. If the past is indicative of the future, we can expect that cost and price analyses will continue to be in great demand. We can also expect that organizations who get ahead of this requirement will enjoy a strategic advantage in government contracting. CM

Christina Graves

- Consultant, Government Contract Services (GCS) practice, Ernst & Young LLP.

- Previously served as a senior auditor for the Defense Contract Audit Agency (DCAA).

- Vice President—Education, Programs, and March Workshops, NCMA Boston Chapter.

The views expressed in this article are solely those of the author and do not necessarily reflect those of Ernst & Young LLP or other members of the global EY organization.

Endnotes

[1] The FAR defines direct costs as those costs that are “identified specifically with a particular final cost objective. Direct costs are not limited to items that are incorporated in the end product as material or labor. Costs identified specifically with a contract are direct costs of that contract. All costs identified specifically with other final cost objectives of the contractor are direct costs of those cost objectives.” (FAR 2.101, “Direct cost” definition.)

[2] The FAR defines indirect costs as “any cost not directly identified with a single final cost objective, but identified with two or more final cost objectives or with at least one intermediate cost objective.” (FAR 2.101, “Indirect cost” definition.)

[3] Editor’s Note: For an in-depth analysis of the process of price analysis, see Thomas Wells’ article, “Price Analysis: The Rules and the Art,” on page 20.

[4] See, generally, FAR 15.403.

[5] I.e., $3 million vs. $2 million—a 33% price difference.

[6] “Professional Development Resources,” Oak Ridge Institute for Science and Education, available at https://orise.orau.gov/resources/stem/professional-development/index.html.

[7] See U.S. Department of Defense, “Contracts,” Defense.gov, available at https://www.defense.gov/Newsroom/Contracts.

[8] I.e., $13.3 million award value ÷ $2 million COPD threshold = 6.65 ≈ 7.

[9] U.S. Bureau of Labor Statistics (BLS), “Occupational Outlook Handbook—Business and Financial: Cost Estimators,” BLS.gov, available at https://www.bls.gov/ooh/business-and-financial/cost-estimators.htm.

[10] I.e., $9,333 = $33.33 × 280 hours; $18,667 = $33.33 × 560 hours.

[11] I.e., $128,000 = $64,000 × 2 employees; $256,000 = 64,000 × 4 employees.

[13] U.S. Department of Defense, “President Signs Fiscal 2019 Defense Authorization Act at Fort Drum Ceremony,” Defense.gov, available at https://www.defense.gov/Explore/News/Article/Article/1601016/president-signs-fiscal-2019-defense-authorization-act-at-fort-drum-ceremony.