Life Cycle Costs: A Guide to Preparing and Executing Contracts

The necessity of management in ensuring reliable life cycle costs in public procurement contracts and the problem of biases.

By Franziska Binder, Ph.D. Candidate; Andreas H. Glas, PD Dr.; and Michael Eßig, Prof. Dr.

Editor’s Note: This article highlights the critical role of Life Cycle Costing (LCC) in contract management for public sector investment goods. This involves crafting contracts that consider long-term value, integrate LCC into procurement, structure for sustained performance, manage life cycle risks, leverage data-driven insights, and foster cross-functional collaboration. By proactively addressing costs beyond acquisition, contract management becomes a strategic driver for fiscal responsibility, ensuring informed, sustainable, and value-oriented outcomes throughout the entire lifespan of public investments. This article provides an in-depth look of LCC and its integral role to public procurement, both at home and abroad.

Editor’s Note: This article highlights the critical role of Life Cycle Costing (LCC) in contract management for public sector investment goods. This involves crafting contracts that consider long-term value, integrate LCC into procurement, structure for sustained performance, manage life cycle risks, leverage data-driven insights, and foster cross-functional collaboration. By proactively addressing costs beyond acquisition, contract management becomes a strategic driver for fiscal responsibility, ensuring informed, sustainable, and value-oriented outcomes throughout the entire lifespan of public investments. This article provides an in-depth look of LCC and its integral role to public procurement, both at home and abroad.

The public sector procures a wide range of investment goods to fulfill its public tasks. (1) These investment goods are used across various sub-sectors, including health care, infrastructure, transportation, communication, energy, and defense. Typically, investment goods are long-lasting, often spanning several decades, and are associated with extensive service requirements such as maintenance, repair, and overhaul. As a result, their total costs are substantial.

Costs along the life cycle of investments often exceed initial investment prices, as acquisition costs typically account for only 20% to 40% of total expenditures, while 65% to 75% of costs arise during the usage phase. (2) To provide a more accurate assessment of long-term financial implications, the estimation of “life cycle cost” (LCC) integrates acquisition costs with all other expenses incurred throughout the investment’s entire or defined life cycle (initiation, design, realization, operation, and end of life). (3)(4)

This comprehensive approach offers a more robust basis for assessing the total costs of an investment good in public procurement. Beyond providing an alternative to purely price-based procurement decisions, LCC information (i.e., LCC and information about variables such as cost drivers or cost escalation) supports more strategic and value-oriented procurement choices, contributing to a long-term perspective in decision-making. (4)(5)

LCC is not a new topic, either for assessing total costs of investment goods or for supporting public decision-makers. The public sector already employs established frameworks for planning and executing investments, (6) methodological guidelines for LCC estimation, and quality assurance measures to enhance the reliability of LCC estimation. (7-9) Additionally, project cost control strategies have been developed to enhance financial oversight. (10)

However, these approaches predominantly focus on the methodological aspects of LCC estimation. They aim to improve LCC estimation reliability, assuming that more precise LCC information leads to “better” decisions in the public sector. Despite decades of use, LCC remains weakly integrated into public procurement decisions. (11-13)

The academic discussion identifies several barriers to its adoption. Decision-makers often lack the expertise and resources to use LCC effectively in decision-making. More recent research highlights behavioral biases as key explanatory factors. (14-16) Bias can be defined as a systematic distortion in judgment, interpretation, and consideration of information that results in misjudgments and suboptimal decisions. (16)

Within LCC estimation, bias manifests in overly optimistic, deliberately inaccurate project assumptions. In the interpretation of LCC information, bias is evident in the perception that such information is unreliable or of limited utility, whereas in the decision-making procedure, bias may result in the intentional understatement of LCC information or an unconscious overreliance on baseline LCC rather than updated LCC information.

To summarize, public decision-makers are influenced by biases that affect LCC estimation and interpretation of LCC information by perceiving LCC as unreliable or unbeneficial. These biases further limit optimal consideration of LCC information and may result in suboptimal procurement decisions.

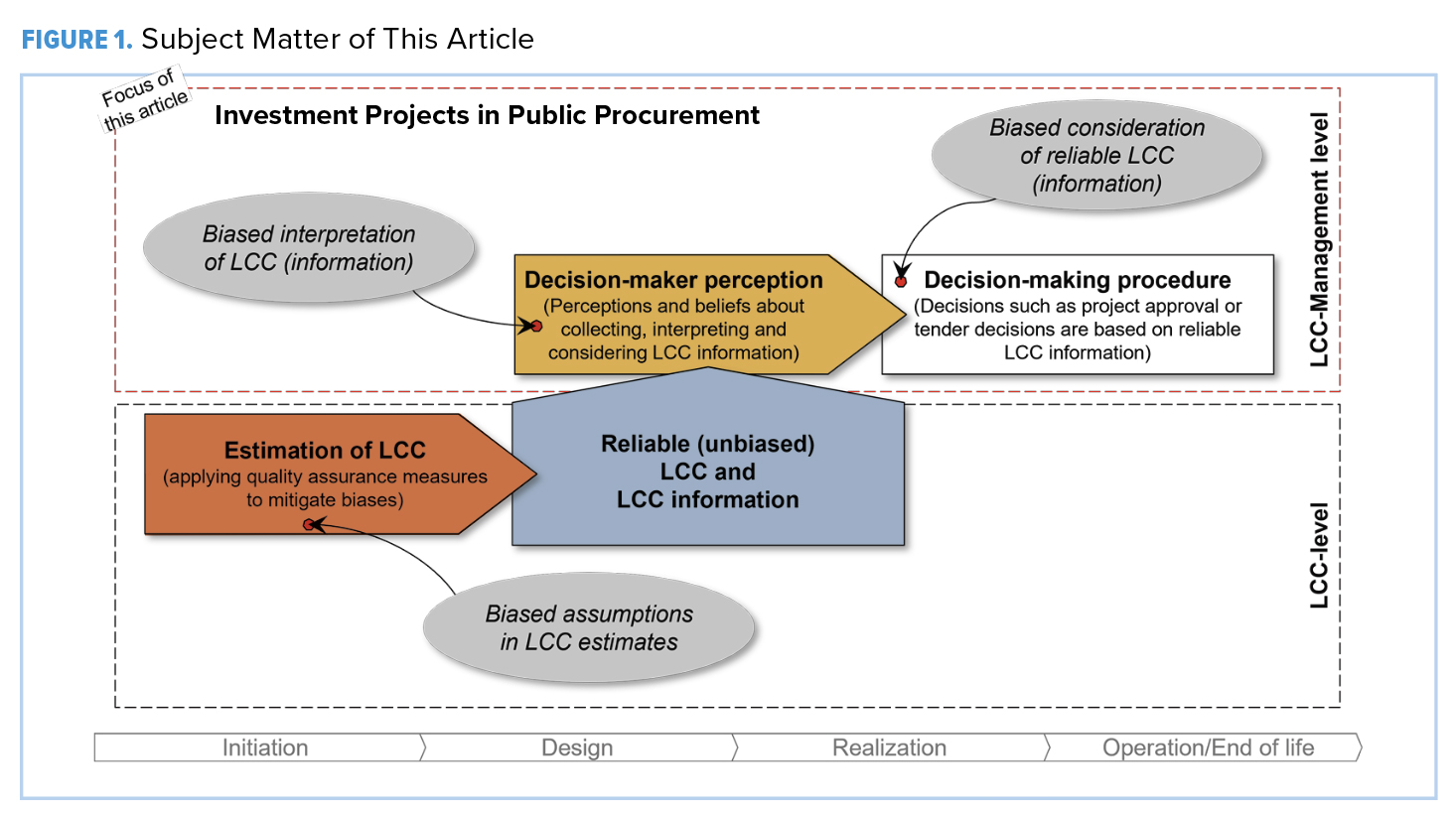

As Figure 1 illustrates, this article specifically addresses this issue at the level of LCC management, as the LCC estimation process is already well-developed through various quality measures designed to mitigate biases. It examines the factors influencing the perception and integration of LCC in public procurement. It explores strategies to mitigate behavioral biases and enhance the perceived reliability and benefits of LCC among public decision-makers.

This article draws on recent research on LCC management and insights from interviews with contracting experts in the public procurement sector. By emphasizing the need for a systematic approach to integrating reliable LCC information more actively into decision-making, this study seeks to identify biases that affect decision-makers’ perceptions of LCC reliability and usefulness, as well as those that influence the consideration of LCC (information) in the decision-making procedure.

The findings contribute to a better understanding of behavioral biases and offer proposals for mitigating them, thereby improving the perception and integration of LCC as a reliable and valuable decision-making tool. A key recommendation is the establishment of a stronger cost culture within public procurement organizations – one that balances political, technical, social, and economic objectives of an investment project based on LCC information. The concept of cost culture encompasses the shared values and norms that define an organization’s approach to LCC, thereby shaping behaviors and influencing decision-making processes. (17)

Regulatory Aspects of LCC Integrity in Public Procurement Decisions

Understanding LCC in Public Procurement

Traditional project delivery models, such as Design-Bid-Build, prioritize initial investment costs, often favoring the lowest bid. (18)(19) However, this short-term cost focus can result in fragmented cost structures and insufficient consideration of long-term fiscal sustainability.

In response, public procurement organizations are increasingly adopting integrated and performance-based models, such as Design-Build and Performance-Based Contracting, which assess costs across the entire project life cycle. (18)(20) These models facilitate enhanced cost control and ensure sustained adherence to project cost goals.

Public sector investments are procured by organizations that operate within a highly formalized and standardized regulatory framework. (21) These organizations must comply with procurement regulations at regional, national, and international levels. For example, procurement authorities within the European Union (EU) are subject to the principles established by EU procurement directives (e.g., Directive 2014/24/EU; Directive 2009/81/EU). These regulatory frameworks not only uphold transparency and ethical integrity but also aim to enhance economic efficiency within the public sector.

To optimize economic efficiency, public procurement organizations are encouraged to apply the “Most Economically Advantageous Tender” criterion, which incorporates not only initial investment costs but also long-term operational and disposal expenses. Consequently, legislators have authorized the integration of LCC into procurement decisions, allowing its use as an award criterion in public tenders (Directive 2014/24/EU, Article 67; Directive 2009/81/EU, Article 47).

Beyond regulatory compliance, and in alignment with the shift toward integrated and performance-based models, public procurement organizations increasingly acknowledge the strategic importance of LCC. (22)(23) Internal regulations and organization-specific guidelines further reinforce the institutionalization of LCC, ensuring systematic integration beyond the initial tendering phase. Consequently, the regulatory environment fosters the integration of the LCC approach, thereby enabling public investments to be embedded within a long-term perspective that goes beyond the short-term budgetary logic.

LCC Integrity in Key Project Milestone Decisions and Cost Performance

The integration of LCC into public procurement serves a dual function, significantly enhancing both the pre-contract and post-contract phases of an investment.

In the pre-contract phase, LCC facilitates comprehensive economic project planning and evaluation by considering the total expenses of an investment. (3)(4) This phase is characterized by multiple iterative LCC estimations and budget adjustments aimed at refining the projected LCC as reliably as possible. LCC serves as a critical decision-support tool (15)(24) by providing a robust analytical cost basis, such as for design requirements decisions, tender evaluations, and contractual negotiations, ensuring well-informed cost planning before reaching key project milestones.

The reliability of the LCC estimates – defined as the extent to which estimates are comprehensive, well-documented, accurate, and credible (7) – has a significant impact on budgeting and contractual arrangements. As illustrated in Figure 2, the reliability of LCC estimates evolves throughout the project life cycle due to variations in data availability (e.g., evolving project design specifications), scope adjustments, and external economic conditions (e.g., changing political legislation). (25)(26)

Thus, a key challenge in the pre-contract phase is the inherent uncertainty of LCC estimations within budget constraints and upcoming contractual agreements. Base LCC estimates often serve as indicative reference points rather than definitive cost commitments. Therefore, cost contingencies (i.e., additional funds incorporated into the base LCC estimate) are frequently considered during contract negotiations to account for unforeseen expenditures. (24)

Beyond project cost estimation, LCC is also recognized as a strategic cost management tool, (27) providing evidence-based insights into the cost dynamics, drivers, and trends of public investments. Therefore, in the post-contract phase, LCC remains an essential instrument for cost monitoring and control across the project’s key milestones. (22)(28)

The contracted LCC serves as a benchmark value against which actual costs are assessed. By systematically tracking and analyzing cost developments, LCC enables proactive cost containment, mitigating unexpected cost escalations and project delays. Additionally, it enables operational efficiency improvements, ensuring that actual expenditures align with projected investment cost plans

The dual function of LCC estimates renders that LCC is not only essential for external use (e.g., contract bidding) but also for internal functions (e.g., monitoring project costs). (5) Consequently, LCC serves as a critical management tool in both the pre-contract and post-contract phases. By systematically applying LCC principles throughout the project’s life cycle phases, public investments can achieve long-term economic efficiency, ensuring that public financial resources are effectively allocated and controlled. LCC information, therefore, plays a pivotal role in shaping the project’s cost performance development.

Cost performance refers to the deviation between initially planned and actual project expenditures. (15) Depending on the point of reference, different project phases may be considered for evaluation. For example, cost deviations can be assessed by comparing the initially forecasted budget (i.e., base LCC estimate) with the contract value (i.e., contracted LCC).

Public investments, however, are frequently subject to systematic cost overruns, a phenomenon observed across various industries and countries. Notable cases, such as the Stuttgart 21 rail project (Germany) and the 2014 Olympic Games in Sochi (Russia), experienced cost overruns from the originally estimated acquisition and realization costs of more than 220%. (29)(30) Similarly, operating costs of the F-35 fighter aircraft program increased by 61.3% between 2018 and 2021. (31) Given these trends, the ability to reliably estimate LCC values and mitigate cost overruns is crucial for the public sector. Reliable LCC estimates are essential not only for the successful execution of individual investments but also for the strategic planning and allocation of public resources across future initiatives. (26)

In response to these challenges, recent research has increasingly focused on advances in quality assurance measures aimed at improving the reliability of LCC estimates. (22)(25)(32) Sensitivity, risk, and uncertainty analyses have become standard tools for assessing potential risks and uncertainties associated with project costs. Additionally, improved information exchange, both internally and externally, has been shown to enhance data accuracy and transparency. Regular LCC estimates updates, combined with independent audits, further refine cost assumptions and reduce estimation errors. Consequently, it can be concluded that, despite the uncertainties associated with LCC estimates, they are not subject to biases.

Despite these methodological improvements, the behavior of procurement officials remains a critical factor influencing the practical implementation of LCC principles. As Ditkaew (2018) emphasizes, effective LCC-based decision-making requires a structured approach involving the rational or rather unbiased generation, evaluation, and consideration of project cost options. (28)

Moreover, a fundamental prerequisite for evidence-based decision-making is the interpretation of LCC information. (33) Decision-makers must not only trust the reliability of LCC data but also recognize its practical relevance for its active consideration and integration into procurement processes. (34)

Empirical evidence suggests that public decision-makers consistently exhibit behavioral biases when making LCC-relevant decisions, thereby influencing both the interpretation and processing of LCC information. In the context of (public) project management, these biases can be classified into “psychological/cognitive” and “strategic/political” categories. (14)(16)

Cognitive biases refer to unconscious, systematic deviations from rational decision-making, whereas strategic biases involve deliberate distortions of information to serve specific objectives. Generally, behavioral biases distort the assessment of LCC information, often resulting in its misinterpretation as unreliable or of limited value. (11-13)(22)

Experimental studies have identified key biases affecting decision-making in the public sector (e.g., healthcare and education), including anchoring bias (i.e., overreliance on specific reference points), status quo bias (i.e., preference for maintaining existing conditions when faced with multiple alternatives), and framing effects (i.e., emphasis on positive developments while downplaying negative aspects). (35-37)

These biases contribute to an excessive reliance on base LCC estimates, resistance to alternative cost considerations, and selective interpretation and processing of cost performance information. Accordingly, decision-makers often fail to effectively integrate LCC principles into their procurement decisions.

Also, further research on project management suggests that behavioral biases impact multiple phases of the procurement process, (14)(38) impairing the objective assessment of LCC-related information. Ultimately, cognitive and strategic biases contribute to reduced decision-making efficiency in public procurement, leading to suboptimal investment decisions and inefficient resource allocation.

Given that prior studies have focused on broader regulated environments without explicitly considering LCC, empirical validation within the regulatory procurement framework is necessary. Such an approach would enable the identification of systematic constraints that hinder LCC adoption and affect its perceived reliability and utility in public procurement. The following section performs such an investigation.

LCC-Based Procurement Decisions: Bias Insights from Interviews

Building on the initial hypothesis that decision-makers exhibit cognitive and strategic biases in interpreting and considering LCC information during decision-making, a series of interviews was conducted in 2024 with 29 contracting experts in the public procurement sector. The experts represented various roles and hierarchical levels (e.g., directors, senior managers, project and program managers) across multiple sectors (e.g., energy, defense and infrastructure) and countries (e.g., Germany, Canada, Luxembourg, Norway and multinational organizations).

Their insights provided a comprehensive perspective on the handling of LCC information, with a particular focus on its interpretation and consideration in procurement decisions across the project life cycle.

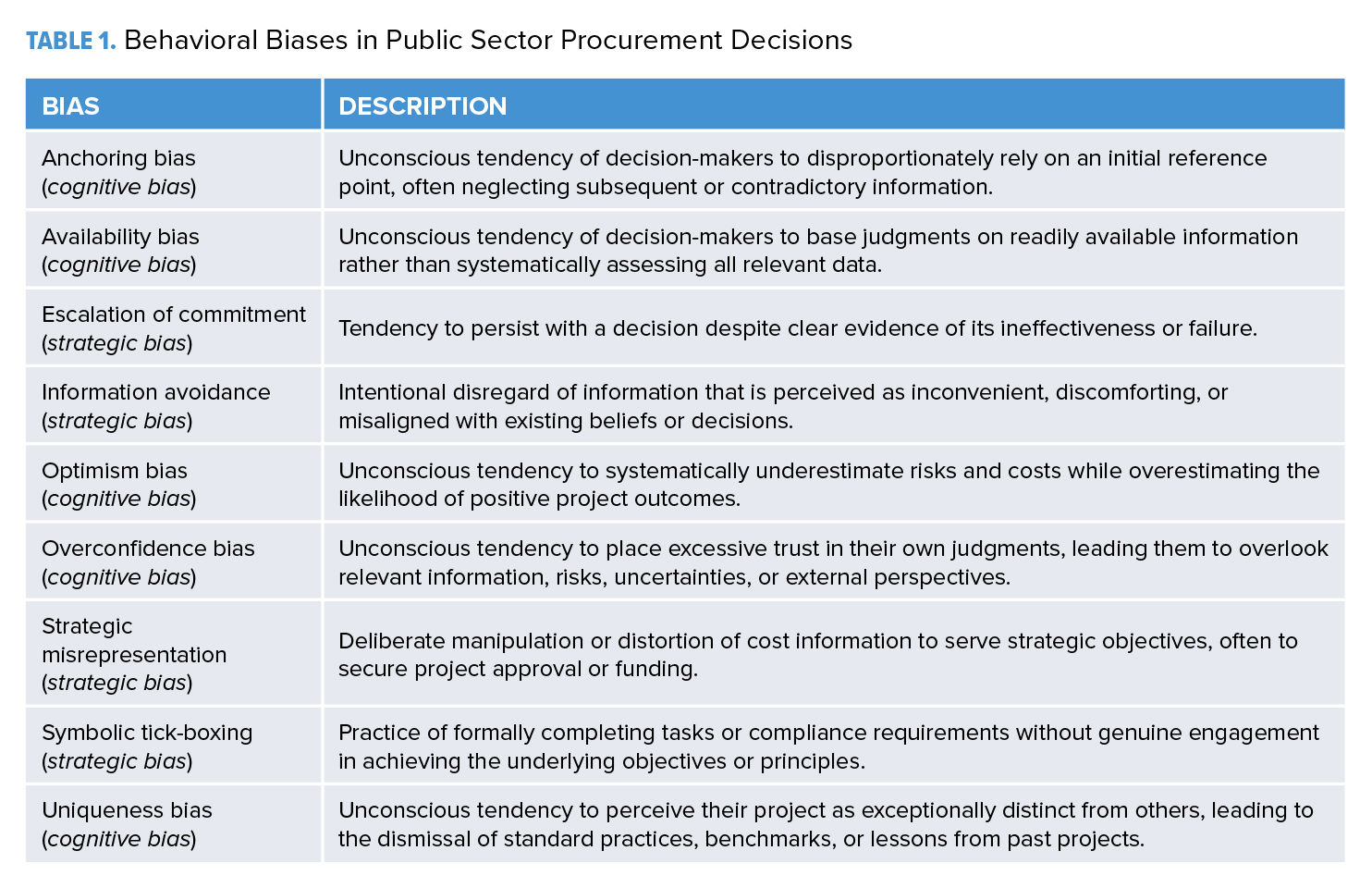

The interviews confirm the presence of nine specific behavioral biases in public procurement: anchoring bias, availability bias, escalation of commitment, information avoidance, optimism bias, overconfidence bias, strategic misrepresentation, symbolic tick-boxing, and uniqueness bias (see Table 1).

These biases persist throughout the project life cycle, shaping the (un)conscious perception and interpretation of LCC information and affecting its systematic integration into procurement decisions. As a result, LCC remains underutilized in long-term cost management and strategic planning, limiting its effectiveness in enhancing economic procurement efficiency.

Not all the identified behavioral biases directly hinder LCC adoption or affect its perceived reliability and utility in public procurement. However, multiple biases contribute to decision-making distortions. Contracting experts report that LCC estimations are often conducted as a “pro forma” requirement, serving as “just a tick in the box” rather than being meaningfully integrated into decision-making (symbolic tick-boxing).

Furthermore, public procurement officials frequently disregard and systematically neglect LCC information (information avoidance). A recurring issue identified by experts is the lack of familiarity with LCC principles and insufficient expertise among decision-makers, leading to the perception that LCC holds little practical relevance. Consequently, procurement decisions are rarely based on LCC considerations.

Additionally, procurement decisions tend to be anchored to initial investment prices and performance metrics rather than LCC considerations (anchoring bias). This prioritization of short-term expenditures over long-term financial efficiency directly obstructs LCC consideration and diminishes its strategic importance in procurement decisions.

Similarly, decision-makers often favor personal experience and intuition over LCC data (availability bias), perceiving them as more trustworthy and reliable sources of information. This reliance weakens confidence in LCC information and reduces their integration into procurement processes.

Collectively, behavioral biases, particularly those related to the processing and interpretation of LCC information, significantly affect the perceived reliability and utility of LCC, ultimately limiting its adoption in public procurement decision-making.

The interview results further indicate that strategic biases are particularly reinforced by the institutional, regulatory, and organizational dynamics of regulated procurement environments. These environments establish structural conditions that can incentivize intentional misbehavior and the misuse of LCC information, ultimately shaping its systematic integration into decision-making.

For example, this study has demonstrated that in a regulated environment, strategic misrepresentation and escalation of commitment are particularly prevalent due to institutional constraints to fulfill public tasks. Short-term priorities, such as rapid project execution and political agendas, often override long-term cost considerations, making objective, LCC-based decision-making increasingly difficult.

Additionally, regulatory complexity fosters symbolic tick-boxing behavior, where LCC is viewed as a bureaucratic requirement rather than a strategic decision-making tool. This results in a preference for simpler decision criteria, such as investment price, which also reflects information avoidance.

Organizational structures further reinforce biases that prevent the systematic integration of LCC in procurement decisions. Frequent personnel turnover disrupts the accumulation of expertise and reinforces short-term decision-making, as decision-makers are rarely accountable for long-term consequences. Annual budget cycles in the public sector fragment cost structures, limiting transparency and making comprehensive LCC reporting difficult as individual project phases are considered in isolation.

As a consequence of the presence of various strategic and cognitive biases in public procurement, the interview findings reveal varying degrees to which LCC information is considered in the decision-making process. While LCC-related information is one of several decision criteria, procurement decisions are often guided by time constraints, performance metrics, supplier stability, and price considerations. (19)(20)

The LCC usage in public sector organizations differs significantly across project phases. In early procurement stages, decision-makers rely primarily on aggregated cost data without detailed consideration of long-term expenses – an approach also evident in project termination decisions.

As projects progress, LCC becomes more relevant, particularly during project approval, realization, and obsolescence management. However, its prioritization remains inconsistent, ranging from full integration to complete neglect. Other factors, such as time and performance, often carry greater weight.

In summary, the interview findings underscore the multifaceted nature of behavioral biases in LCC-based procurement decisions within the public sector. These insights highlight the critical need to address these biases to ensure the effective interpretation and consideration of LCC principles into procurement decision-making. Without targeted strategies to mitigate behavioral biases and address institutional barriers, LCC will remain underutilized, limiting its potential to enhance long-term cost considerations in public procurement.

Indications of Strategies to Debias Decision-Maker Behavior in Public Procurement

The expert interviews indicate that insufficient knowledge about LCC is a primary barrier to its reliability, utility and integration in decision-making procedures. Without a clear understanding of its value and application, decision-makers struggle to develop trust in LCC information, limiting its perceived reliability and usefulness, and thus consideration.

Consequently, targeted training and knowledge enhancement represent the most fundamental debiasing strategy to bridge this gap. (39) Additional debiasing strategies include incentivizing and motivating organizational members, as well as enhancing evidence-based decision-making through the transparent sharing of LCC information across organizational units. Furthermore, the implementation of comprehensive LCC reporting is essential to ensure transparency and trust. (25)(32)(37)

However, isolated debiasing measures are unlikely to produce sustained improvements in LCC interpretation and consideration. Instead, an integrative and holistic approach is necessary, one that strengthens cost culture and embeds LCC principles at multiple levels within public procurement organizations.

Cost culture refers to the shared values and norms that shape an organization’s approach to costs and have a direct impact on behaviors and decision-making processes. (17) A strong cost culture not only fosters greater LCC consciousness but also enhances organizational performance and cost efficiency. (17)(40)

Thus, reinforcing cost culture is central to improving decision-makers’ perception regarding the reliability and utility of LCC information and ensuring its active integration in decision-making. To strengthen cost culture in public procurement organizations, three key strategies are essential: leadership commitment, structured LCC management approach, and empowering organizational members: (41)

• At the leadership level, embedding LCC principles in procurement processes requires clear cost objectives, transparent communication, and long-term procurement planning. Leaders must act as role models, promoting LCC consciousness and ensuring that LCC information is systematically shared across departments and is accessible to decision-makers. Strong leadership commitment legitimizes the use of LCC and helps establish it as a central element of procurement strategy.

• A well-defined and structured approach to LCC management is critical. Standardized LCC estimation methods and continuous cost monitoring facilitate early detection of cost deviations, enabling the timely implementation of cost containment actions. Ensuring easy access to LCC manuals and guidelines further supports the consistent application of LCC estimation. Additionally, clear reporting mechanisms improve transparency across all project phases, strengthening confidence in LCC information and promoting its systematic use.

• Finally, empowering organizational members through targeted training and incentives is crucial for sustained LCC interpretation and consideration. Training programs should address common misconceptions and emphasize the strategic benefits of LCC-based decision-making. Moreover, incentive structures aligned with cost-efficiency goals can reinforce long-term commitment to LCC principles. Given the frequent turnover in public organizations, maintaining institutional knowledge continuity is essential to avoid repeated knowledge gaps that hinder LCC understanding and implementation.

This shift toward a stronger cost culture requires a long-term commitment to transforming organizational mindsets, as resistance from procurement officials accustomed to traditional cost structures may pose a challenge. Early interventions are necessary to establish LCC as a core strategic consideration rather than a peripheral reporting obligation.

Final Considerations and Conclusion

The study’s findings offer empirical evidence that a robust methodological framework alone is insufficient to ensure that procurement officials in the public sector perceive LCC information as reliable and useful, and that it is integrated into public procurement decision-making. A holistic approach is required – one that integrates LCC principles throughout the entire procurement process and enables proactive cost management rather than reactive adjustments. The findings emphasize that merely providing reliable LCC information does not guarantee its effective use; instead, its perceived reliability and utility depend on how well procurement officials embed LCC into their decision-making processes.

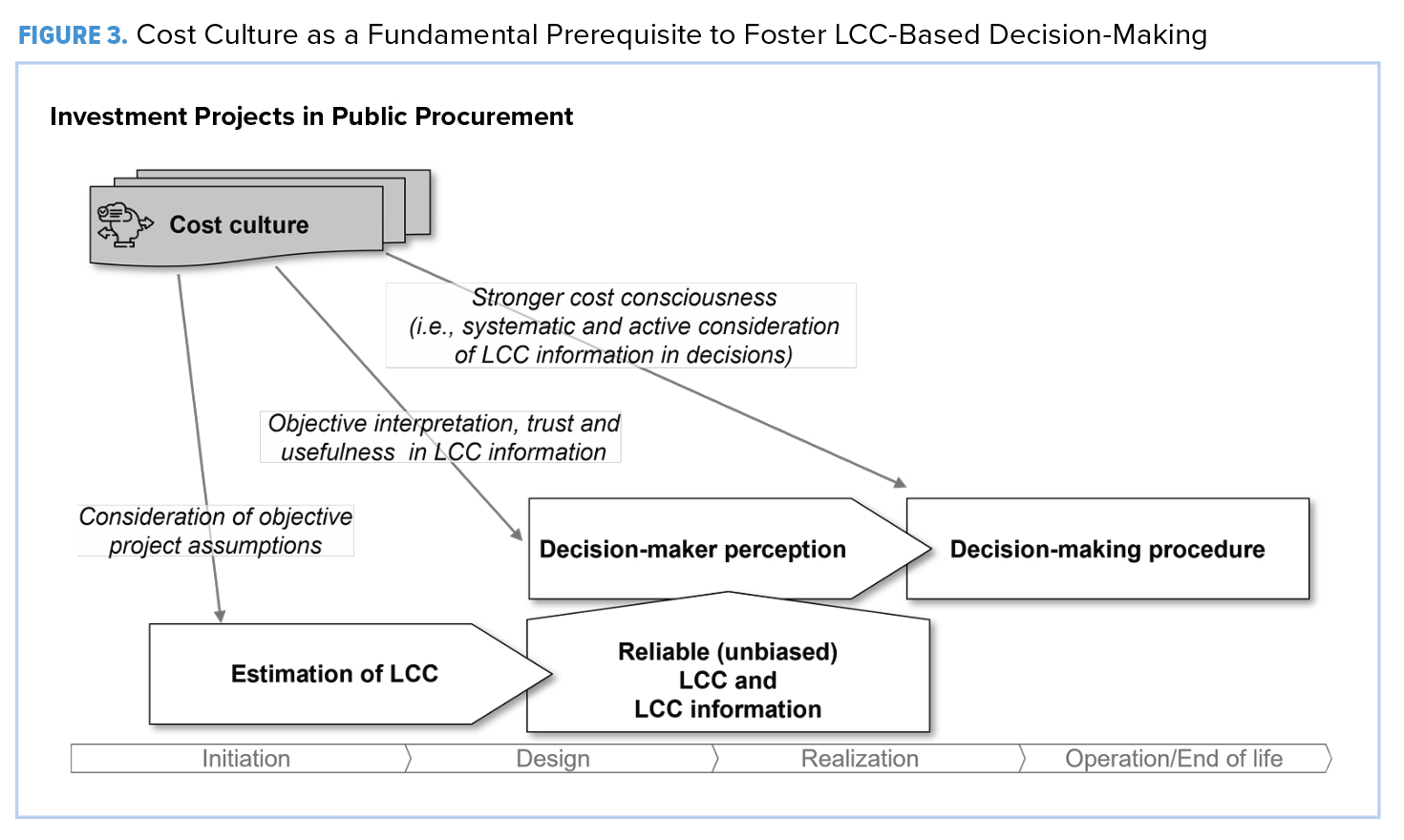

Figure 3 reinforces this key conclusion, highlighting that cost culture serves as a fundamental prerequisite for the unbiased estimation of LCC and, in particular, the systematic and unbiased interpretation and consideration of LCC in public procurement. Strengthening cost culture at multiple levels – leadership, LCC management, and organizational members – is critical to fostering trust in LCC information and ensuring its meaningful integration into decisions.

Further, the model underscores the constant interdependence between LCC estimation and LCC management. While reliable cost estimation is especially essential for procurement planning and tendering, continuous cost management throughout the project life cycle is equally important for maintaining economic efficiency. Without sustained cost monitoring, control, and containment, contracted LCC can become strategically irrelevant. This increases the likelihood of cost inefficiencies and misallocations in procurement decisions.

To establish greater trust in the reliability and usefulness of LCC information, and to ensure its systematic integration in public investment decisions, procurement organizations must establish a cohesive link between LCC estimation, management, and decision-making.

This requires not only methodological improvements in transparent LCC reporting and proactive cost management mechanisms but also a cultural shift that embeds LCC consciousness across procurement structures. Without this transformation, the potential benefits of LCC remain underutilized, limiting its impact on long-term economic efficiency in public procurement. CM

Franziska Binder is a research associate and doctoral candidate at the Procurement Research Group at the University of the Bundeswehr Munich since December 2020. Her academic work focuses on the reliability of life cycle cost management in public procurement, with special emphasis on establishing a well-developed cost culture in public procurement organizations.

Andreas H. Glas, PD Dr. is Managing Director of the Defence Acquisition & Supply Management Competence Center and Co-Head of the Procurement Research Group at the University of the Bundeswehr Munich since 2020. He earned his doctorate with a dissertation on Performance-Based Contracting and completed his habilitation in 2019 on strategic procurement for emergency organizations and armed forces. Currently, together with his research group, he is investigating various issues related to the further development of defence supply management, including the use of 3D printing, smart contracting, performance-based logistics, parallelization of planning processes, and the Defence Industry Compass sector study.

Michael Eßig, Prof. Dr. holds the Chair of General Business Administration, with a particular focus on Procurement and Supply Management, and is the head of the Procurement Research Group at the University of the Bundeswehr Munich. His research focuses on strategic procurement, public procurement, and procurement management in the defense sector. In this context, he specializes in innovation and digitalization in procurement management, incentive-based supplier management, and the value contribution of procurement. His publications include contributions to renowned academic journals such as the Journal of Cleaner Production, the Journal of Purchasing and Supply Management, and the Journal of Public Procurement, for which he also serves as co-editor.

ENDNOTES

1 OECD: Government at a Glance 2023, 2023.

2 GAO-09-3SP: GAO Cost Estimating and Assessment Guide: Best Practice for Developing and Managing Capital Program Costs, 2009.

3 Woodward D.G. (1997): Life cycle costing-theory, information acquisition and application. International Journal of Project Management; 15 (6): 335–44.

4 Taylor W.B. (1981): The use of life cycle costing in acquiring physical assets. Long Range Planning; 14 (6): 32–43.

5 Asiedu Y., Gu P. (1998): Product life cycle cost analysis: State of the art review. International Journal of Production Research; 36 (4): 883–908.

6 BMDV: Leitfaden Großprojekte, 2018.

7 GAO-20-195G: Cost Estimating and Assessment Guide: Best Practice by Developing and Managing Program Cost, 2020.

8 SRD: NATO Life Cycle Costs Common Methodology: NATO SRD ALCCP-1.1, 2022

9 ALCCP-01: NATO Guidance on Life Cycle Costs, 2018.

10 HM Treasury: The Green Book: Central Government Guidance on Appraisal and Evaluation, 2020.

11 Nucci B., Iraldo F., De Giacomo M.R. (2016): The relevance of Life Cycle Costing in Green Public Procurement. Economics and policy of energy and the environment (1): 91–109.

12 Higham A., Fortune C., James H. (2015): Life cycle costing: evaluating its use in UK practice. Structural Survey; 33 (1): 73–87.

13 Olubodun F., Kangwa J., Oladapo A., et al (2010): An appraisal of the level of application of life cycle costing within the construction industry in the UK. Structural Survey; 28 (4): 254–65.

14 Flyvbjerg B. (2021): Top Ten Behavioral Biases in Project Management: An Overview. Project Management Journal; 52 (6): 531–46.

15 Love P.E.D., Irani Z., Smith J., et al (2017): Cost performance of public infrastructure projects: the nemesis and nirvana of change-orders. Production Planning & Control; 28 (13): 1081–92.

16 Ika L., Pinto J.K., Love P.E.D., et al (2023): Bias versus error: why projects fall short. Journal of Business Strategy; 44 (2): 67–75.

17 Diefenbach U., Wald A., Gleich R. (2018): Between cost and benefit: investigating effects of cost management control systems on cost efficiency and organisational performance. Journal of Management Control; 29 (1): 63–89.

18 Aliza A.H., Stephen K., Bambang T. (2011): The Importance of Project Governance Framework in Project Procurement Planning. Procedia Engineering; 14: 1929–37.

19 de Araújo M.C.B., Alencar L.H., Miranda Mota C.M. de (2017): Project procurement management: A structured literature review. International Journal of Project Management; 35 (3): 353–77.

20 Brown D.C., Ashleigh M.J., Riley M.J., et al (2001): New Project Procurement Process. Journal of Management in Engineering; 17 (4): 192–201.

21 Csaki C. (2006): Investigating the decision making practice of public procurement procedures. 2nd International Public Procurement Conference Proceedings in Rome (21.-23. September 2006) Paper 35: 869–99.

22 Brandstetter M., Binder F., von Deimling C., et al (2023): Life cycle cost in public procurement: Insights from a survey taking the supplier’s perspective. 32nd IPSERA Conference “Systemic Change” at EADA Business School Barcelona (2.-5. April 2023) Paper 7719: 1–21.

23 Knauer T., Möslang K. (2018): The adoption and benefits of life cycle costing. Journal of Accounting & Organizational Change; 14 (2): 188–215.

24 Love P.E.D., Zhou J., Edwards D.J., et al (2017): Off the rails: The cost performance of infrastructure rail projects. Transportation Research Part A: Policy and Practice; 99: 14–29.

25 Love P.E.D., Smith J., Simpson I., et al (2015): Understanding the Landscape of Overruns in Transport Infrastructure Projects. Environment and Planning B: Planning and Design; 42 (3): 490–509.

26 Flyvbjerg B. (2007): Cost Overruns and Demand Shortfalls in Urban Rail and Other Infrastructure. Transportation Planning and Technology; 30 (1): 9–30.

27 Ellram L.M., Tate W.L. (2016): The use of secondary data in purchasing and supply management (P/SM) research. Journal of Purchasing and Supply Management; 22 (4): 250–54.

28 Ditkaew K. (2018): The Effects of Cost Management Quality on the Effectiveness of Internal Control and Reliable Decision-Making: Evidence from Thai Industrial Firms. Advances in Social Science, Education and Humanities Research; 211: 60–69.

29 Steininger B.I., Groth M., Weber B.L. (2021): Cost overruns and delays in infrastructure projects: the case of Stuttgart 21. Journal of Property Investment & Finance; 39 (3): 256–82.

30 Flyvbjerg B., Stewart A., Budzier A. (2016): The Oxford Olympics Study 2016: Cost and Cost Overrun at the Games. Saïd Business School Research Paper 2016-20.

31 GAO-21-439: F-35 Sustainment: DOD Needs to Cut Billions in Estimated Costs to Achieve Affordability, 2021.

32 Aibinu A.A., Pasco T. (2008): The accuracy of pre-tender building cost estimates in Australia. Construction Management and Economics; 26 (12): 1257–69.

33 Citroen C.L. (2011): The role of information in strategic decision-making. International Journal of Information Management; 31 (6): 493–501.

34 Oduyemi O., Okoroh M., Fajana O.S. (2016): Risk assessment methods for life cycle costing in buildings. Sust. Build; 1 (3).

35 Bellé N., Cantarelli P., Belardinelli P. (2018): Prospect Theory Goes Public: Experimental Evidence on Cognitive Biases in Public Policy and Management Decisions. Public Administration Review; 78 (6): 828–40.

36 Nagtegaal R., Tummers L., Noordegraaf M., et al (2020): Designing to Debias: Measuring and Reducing Public Managers’ Anchoring Bias. Public Administration Review; 80 (4): 565–76.

37 Cantarelli P., Bellé N., Belardinelli P. (2020): Behavioral Public HR: Experimental Evidence on Cognitive Biases and Debiasing Interventions. Review of Public Personnel Administration; 40 (1): 56–81.

38 Patrucco A.S., Bellis P., Trabucchi D., et al (2024): Behavioral Biases and Cognitive Pitfalls: Navigating Resource Orchestration in Supplier-Partnered Innovation Projects. IEEE Transactions on Engineering Management: 1–15.

39 Binder F., von Deimling C., Eßig M. (2023): Impact of training on the maturity of life-cycle cost knowledge: A contribution to cost culture in a regulated procurement environment? der moderne staat – Zeitschrift für Public Policy, Recht und Management; 16 (2): 507–35.

40 Himme A. (2012): Critical success factors of strategic cost reduction. Journal of Management Control; 23 (3): 183–210.

41 Binder F., von Deimling C., Eßig M.: Kostenkultur in regulierten Beschaffungsumgebungen: Ein Ansatz zur Reduzierung von systematischen Kostenabweichungen bei Großprojekten?, in: Lebenszykluskostenmanagement: Strategische (Kosten-) Steuerung komplexer Beschaffungsvorhaben. Edited by Eßig M., von Deimling C., Springer Gabler, (in press).